A Simple Alternative to Alternatives?

- Many sophisticated investors have incorporated alternative assets into their portfolios to enhance risk-adjusted returns. In doing so, they have accepted reduced liquidity and increased portfolio complexity. The results have been mixed.

- The 60/40 portfolio structure has been a dominant investment approach for decades, but its forward-looking efficacy has been increasingly debated in recent years.

- Simple, liquid 60/40 portfolio structures have generated strong returns in recent years, and we believe this is likely to continue.

- For investors willing to broaden the toolkit, a thoughtfully constructed blend of active public equity and intermediate-duration fixed income can offer meaningful diversification benefits alongside an attractive risk-return profile.

Introduction: Revisiting the 60/40 Paradigm

The conceptual underpinnings of the 60/40 portfolio date back to the 1950s, following the development of Modern Portfolio Theory by American economist and Nobel laureate Harry Markowitz. Markowitz demonstrated that combining financial assets with low or negative correlations could improve risk-adjusted returns. While he did not argue for any specific asset class or allocation, the 60/40 approach later became a practical translation of his theory: public equities and government bond markets offered high liquidity and relatively low correlation to one another.

Strong performance across multiple market cycles further validated the 60/40 approach. US Treasury yields peaked in 1981, marking the beginning of a multi-decade bond bull market, while US equities benefitted from disinflation and strong growth in the economy. Importantly, bonds also demonstrated their diversification benefits by delivering positive returns during both the dot-com bubble and the 2008 financial crisis.

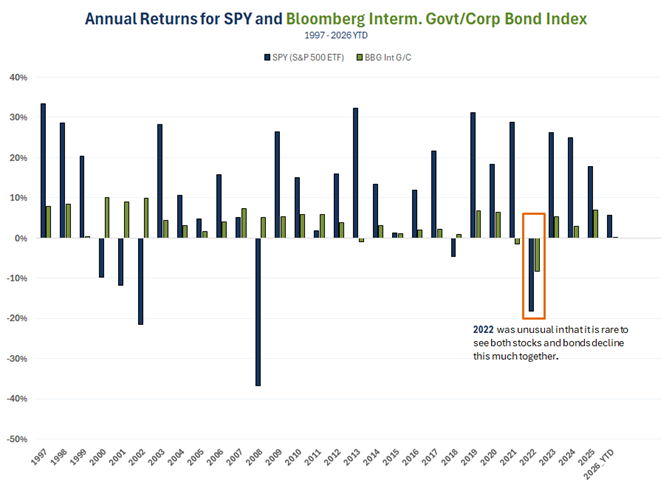

Figure 1: Stock and Bond Annual Returns

Source: JAG Research, FactSet

Despite its strong historical track record, the 60/40 approach has come under increased scrutiny since 2022. As inflation surged and central banks raised interest rates aggressively that year, both stocks and bonds declined simultaneously, leaving investors with “no place to hide” (Figure 1). This also raised questions about the increasing correlation between stocks and bonds, which could erode the diversification benefits of a 60/40 portfolio. BlackRock, for example, dubbed 2022–2024 a “new regime,” in which 60/40 portfolios delivered lower returns and higher stock-bond correlation versus the prior decade. As a result, investors increasingly sought additional sources of diversification, contributing to greater interest in alternative investments.

Alternative Investments: Potential Benefits, Mixed Results

Alternative investments encompass a wide range of asset classes, including private equity, private credit, hedge funds, real estate, and commodities. Proponents of alternatives point to their potential to deliver enhanced returns and diversification benefits, as these investments tend to exhibit lower correlations to public markets. In addition, certain alternative assets offer predictable cash flows and are viewed as a hedge against inflation.

While some top-tier alternative managers have delivered strong long-term results, the broader empirical evidence on alternative investments leaves significant room for debate. Comparing public and private market returns and volatility presents unique challenges. These include shorter and less consistent data histories versus public markets, less stringent regulatory requirements and lower transparency, infrequent pricing updates due to illiquidity, and the presence of survivorship bias in reported performance data.

In particular, infrequent pricing updates due to illiquidity can have a meaningful impact on how risk and return are perceived. This valuation lag often smooths returns and understates volatility, creating the impression that alternative investments offer a more attractive risk-return profile than public markets. Cliff Asness, co-founder of AQR Capital Management, refers to this phenomenon as “volatility laundering,” where reported risk understates the underlying economic risk of the asset. As Asness wrote in 2023, “The illiquidity and non-marking that came with private investments was appropriately acknowledged as a bug” for much of the history of institutional investing, but in recent years it has increasingly been treated as a feature.

While this “hidden” volatility is generally not an issue in benign market environments, it can quickly surface during periods of market stress as liquidity tightens and valuations are forced to catch up. In 2025 and 2026, private credit markets have been roiled by increasing investor redemption requests, which caused many of the largest funds to limit investor withdrawals. In this episode, private credit concerns have largely been tied to rising worries about AI disrupting software and SaaS business models. Although these fears have been increasingly reflected in liquid public markets, they have not yet been fully reflected in private markets.

The practical implications of these liquidity dynamics extend well beyond private credit. Our colleague James Sindelar recently authored “A Framework for Liquidity Management in Institutional Portfolios,” which discusses how allocations to private markets have shifted what was once a background consideration to the center of portfolio decision-making. As Sindelar notes, liquidity “is not simply a constraint. It is a strategic asset.” We agree, and we believe that liquidity premium should be a central consideration whenever investors evaluate the tradeoffs between public and private allocations.

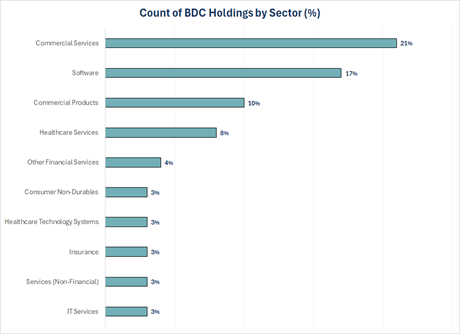

Figure 2: Private Credit Exposure by Sector

Source: PitchBook, JAG Research

Where empirical research is available, findings on alternative investment performance are mixed. The Managed Funds Association (MFA), the trade association for the global alternative asset management industry, has highlighted that incorporating alternative investments materially improved risk-adjusted performance over a recent 25-year period, delivering a 0.73 Sharpe ratio versus 0.56 for a 60/40 blend of the S&P 500 and the Bloomberg US Aggregate Bond Index. Similarly, Hossein Kazemi, Professor of Finance at the University of Massachusetts Amherst, has found that university endowments, which often have a sizable exposure to alternative investments, outperformed global 60/40 portfolios over longer time horizons.

On the other hand, a 2025 study published by the CFA Institute concluded that “adding other alternative assets to the mix … did not result in the anticipated benefits of diversification.” Richard Ennis, a veteran institutional investment consultant, also argues that endowments have historically underperformed public pension plans on a risk-adjusted basis, in large part due to the materially higher costs of many alternative investment vehicles. In a widely cited 2021 study, Ennis calculated that large US endowments underperformed a passive benchmark by roughly 1.6 percentage points per year over the decade following the Global Financial Crisis, an opportunity cost he attributes largely to fees and complexity.

Finally, it is important to differentiate between “real returns” and “paper returns” when analyzing more recent performance for alternative investments. According to an analysis by J.P. Morgan, the total value of unrealized investments held by private equity and venture capital funds has been steadily rising over the past ten years. In the interim, the returns of these investments are calculated using mark-to-market prices that are subjective in nature and determined by the fund’s sponsor.

These circumstances help explain why, despite rising assets under management, distributions by PE and VC funds have been largely flat in recent years. The internal rates of return (IRRs) that investors ultimately realize will be heavily influenced by the exit prices of currently unrealized investments when they are monetized. The combination of longer holding periods, higher borrowing costs, and tough comparisons versus public equity benchmarks collectively creates a high hurdle for alternative managers.

Figure 3: Performance for Select Endowments/Pensions

A Simple, Active 60/40 as a Practical Alternative

Overall, we do not see compelling evidence that alternative investments have consistently outperformed a thoughtfully constructed, actively managed 60/40 portfolio. Given that alternative assets also entail greater complexity, lower transparency, and higher fees, we believe the traditional 60/40 allocation remains the most effective framework for most investors.

We believe a disciplined combination of large-capitalization US growth equities and intermediate-duration core fixed income provides a durable framework for balanced portfolio construction. The equity sleeve is designed to serve as the long-term growth engine, seeking companies that exhibit superior growth characteristics, strong fundamentals, and compelling price appreciation potential. The fixed income sleeve is designed to provide a steady income stream and dampen overall portfolio volatility, typically through a diversified mix of corporate, government, and agency securities with a modest corporate overweight for additional yield.

Backed by decades of empirical evidence and practical experience, we believe the 60/40 framework continues to represent one of the most robust and defensible approaches to balanced investing. It delivers the diversification benefits that investors seek from alternatives, while preserving liquidity, transparency, and cost efficiency. In a market environment where the case for alternatives is increasingly contested, a simple, liquid, active 60/40 allocation may in fact be the most sophisticated choice of all.

Thank you for your interest in JAG Capital Management. We look forward to the opportunity to engage further.

– JAG’s Growth Equity Research Team

—

About JAG

JAG Capital Management (JAG) actively invests for institutions and individuals in highly selective, customizable, and nimble equity and fixed income strategies. JAG is a boutique, independent, employee-owned investment management firm in St. Louis.

Disclosures

This report was prepared by the staff of JAG Capital Management, LLC, an SEC-registered investment adviser. The information herein was obtained from various sources, including but not limited to FactSet, Bloomberg, Reuters, Standard & Poor’s, PitchBook, the Managed Funds Association, the CFA Institute, AQR Capital Management, ChatGPT, Claude, J.P. Morgan, BlackRock, NACUBO, Center for Retirement Research, and the United States Bureau of Labor Statistics, and is believed to be reliable; however, we do not guarantee its accuracy or completeness. The information in this report is given as of the date indicated. We assume no obligation to update this information, or to advise on further developments relating to securities discussed in this report. The opinions expressed are those of the adviser listed above as of the date of this report and are subject to change without notice. The opinions of individual representatives may not be those of the Firm. Additional information is available upon request.

The information contained in this document is prepared and circulated for general information only. It does not address specific investment objectives, or the financial situation and the particular needs of any recipient. Investors should not attempt to make investment decisions solely based on the information contained in this communication, as it does not offer enough information to make such decisions and may not be suitable for your personal financial circumstances. You should consult with your financial professional prior to making such decisions. For institutional investors: JAG Capital Management, LLC, has a reasonable basis to believe that you are capable of evaluating investment risks independently, both in general and with regard to particular transactions or strategies. For institutions who disagree with this statement, please contact us immediately.

Past performance should not be considered indicative of future performance. Any investment contains risk including the risk of total loss.

This document does not constitute an offer, or an invitation to make an offer, to buy or sell any securities discussed herein. J.A. Glynn & Co., JAG Capital Management, LLC, and its affiliates, directors, officers, employees, employee benefit programs, and discretionary client accounts may have a position in any securities listed herein.

A Veteran Owned Business (VOB) is a business owned (51% ownership or greater) by a Veteran who has met the definition of a veteran. The following represents the criteria that the National Veteran Business Development Council (NVBDC) uses in determining ownership:

Ownership: Fifty-one percent ownership by a Veteran or Veterans. The applicant must share in all risk and profits commensurate with their ownership interest.

Control and Management: Proof of active management of the business. Veteran must possess the power to direct or cause to direct the management and policies of the business.

Contribution of Expertise and Capital: Contribution of capital and/or expertise by Veteran owner(s) to acquire their ownership interest shall be real and substantial and be in proportion of the interest acquired.

Independence: The Veteran owner(s) shall have the ability to perform in their area of specialty/expertise without substantial reliance on non-Veteran-owned businesses.