As high school seniors walk across the stage this spring and prepare for life on a college campus, many families are focused on immediate expenses: tuition, dorm supplies, meal plans, and orientation fees just to name a few. But graduation season is also the perfect reminder that higher education planning does not end when college begins. For those with a 529 College Savings Plan, the planning has really just begun.

For younger families watching this year’s graduates take the next step, there is no time like the present to begin saving for future educational costs through a 529 college savings plan. The earlier families begin contributing, the greater opportunity those funds have to grow over time.

The Rising Cost of Higher Education

College costs continue to climb nationwide. Tuition, housing, books, and other educational expenses can place significant financial pressure on families and students alike. While scholarships and financial aid may help offset some expenses, many students still graduate with substantial student loan debt.

That reality is prompting more parents and grandparents to plan earlier, and more intentionally, for future education costs.

A 529 plan offers families a tax-advantaged way to save for qualified educational expenses while allowing investments the opportunity to grow over time.

What Is a 529 Plan?

A 529 plan is a state-sponsored education savings account designed specifically for education-related expenses. Contributions are made with after-tax dollars, but earnings grow tax-deferred, and withdrawals are generally tax-free when used for qualified education expenses.

Qualified expenses may include:

- College tuition and fees

- Room and board

- Books and supplies

- Computers and educational technology

- Certain K-12 tuition expenses

- Apprenticeship programs

- Student loan repayment (subject to limits)

Many states also offer additional state income tax benefits for contributions to their plans.

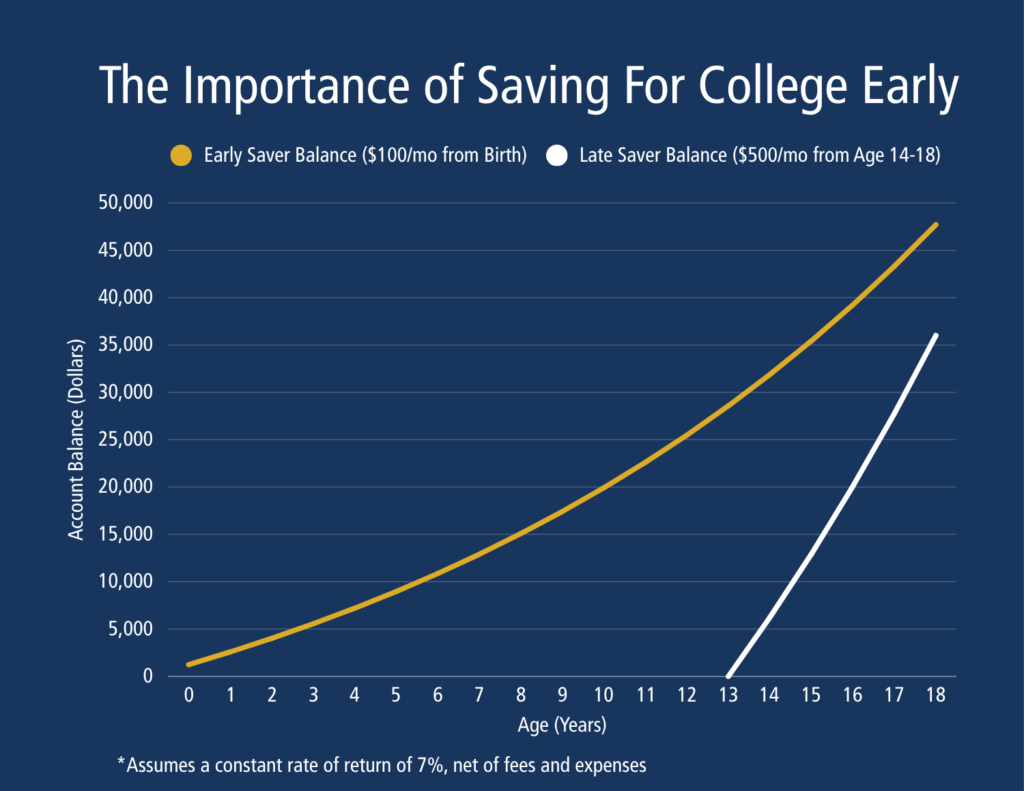

Why Starting Early Matters

One of the greatest advantages of a 529 account is time.

Even modest monthly contributions can grow meaningfully over the course of 10 to 18 years through compounded investment growth. Families who start saving when a child is young may ultimately need to contribute far less out-of-pocket later.

For example, saving $100 per month beginning at birth can create a substantially different outcome than attempting to save aggressively during a student’s high school years.

Graduation season has a way of reminding parents that childhood moves faster than compound interest.

529 Plans Are More Flexible Than Many Families Realize

Some families hesitate to open a 529 account because they worry the child may not attend college or may receive scholarships. However, today’s 529 plans offer significantly more flexibility than many people realize.

Unused funds may often be:

- Transferred to another qualifying family member

- Used for graduate school

- Applied toward vocational or technical education

- Used for qualifying apprenticeship programs

- Rolled into a Roth IRA for the beneficiary under certain conditions and limitations

This flexibility has made 529 plans an increasingly attractive planning tool for many families.

The Best Time to Start Is Now

Watching graduates celebrate their accomplishments often causes younger families to think ahead about their own children’s futures. While college may seem far away, education planning benefits most from consistency and time.

Starting early does not require a large initial investment. What matters most is establishing a plan and contributing consistently over time.

As another class of seniors begins its next chapter, families with younger children have an opportunity to begin building toward theirs.

For more information on 529 Plans, please Contact Us or check out the 529 Plan FAQ Page on the IRS website for more questions and answers.