February 2026

Investing in Transformation That Matters

Software at the AI Crossroads

- SaaS (Software as a Service) stocks have come under increasing pressure as AI tools such as Anthropic’s Cowork have stoked concerns around commoditization and slower seat growth.

- Many software companies will continue to thrive and create attractive opportunities for investors, but the gap between winners and losers is likely to widen significantly.

- JAG’s process does not attempt to time the bottom in SaaS stocks; we will evaluate entry points when and if business momentum and relative strength meaningfully improve.

A Changing Landscape for Software

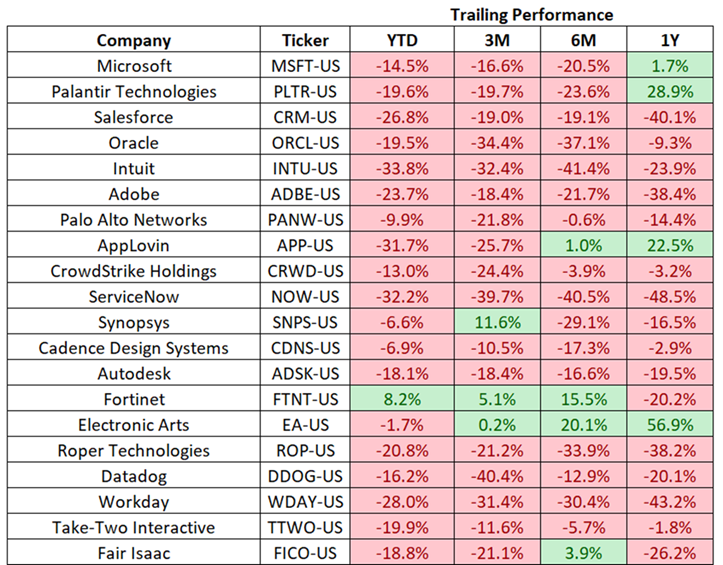

Software stocks are off to a challenging start in 2026, with the industry’s underperformance reminiscent of the sharp drawdown in late 2022. The iShares Expanded Tech-Software Sector ETF (IGV), which tracks North American software companies, is down almost 20% YTD through 2/9/2026. Many of the fund’s holdings have experienced substantially deeper drawdowns. Zooming out, the pain felt by software investors has been evident since mid-2025. On a relative basis, the IGV has been a consistent laggard versus both the S&P 500 and Russell 1000 Growth indexes dating back to May of last year.

Figure 1: IGV Largest Holdings Performance

AI disruption concerns are at the core of recent underperformance. While many tech-related disruptions initially impact specific parts of a business model, AI has the potential to reshape the entire investment framework surrounding SaaS. Investors now must contend with rising commoditization risk, potential pressure on seat-based growth, weakening pricing power, and uncertainty around sustainable growth rates and terminal value assumptions. Collectively, these issues introduce what economists describe as Knightian uncertainty. Originally coined by economist Frank Knight in 1921, Knightian uncertainty refers to situations in which it is difficult (if not impossible) to assign reliable probabilities to a wide variety of potential outcomes. This is particularly true today, as AI models continue to advance at breakneck speed.

In addition to direct business model risks, AI concerns have also introduced greater scrutiny of SaaS management practices – particularly surrounding stock-based compensation (SBC). Atlassian (TEAM), a leading work management and collaboration software provider, is a clear example. In the most recent quarter, the company reported 27.1% non-GAAP operating margin, while GAAP operating margin was (3%). The unusually wide gap is primarily driven by elevated SBC. Investors historically tolerated high SBC in software companies, given durable double-digit revenue growth and 80%+ gross margins. However, as both growth and pricing power come into question, management teams will likely be forced to align incentives more closely with shareholders.

Finally, the AI buildout is proving to be very capital-intensive and requires significant resource allocation from the world’s largest tech enterprises. Alphabet (GOOGL) and Amazon (AMZN) alone announced they will spend a combined $380B on capex in 2026, with the majority of the spend directed towards data centers/AI. This prioritization will also likely exert pressure on IT budgets that otherwise would be directed towards software.

JAG’s Positioning and Perspective

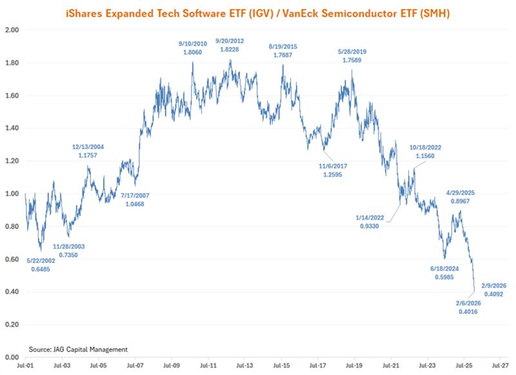

JAG’s Large Cap Growth (LCG) strategy has maintained selective exposure to software, but we remain underweight versus the Russell 1000 Growth benchmark. This positioning reflects our higher conviction in companies leveraged to the AI buildout, which we have predominantly expressed through our positions in semiconductor-related companies. Additionally, we have reduced or exited several positions in recent months in accordance with our sell discipline as relative strength and investor sentiment continued to deteriorate.

Figure 2: Software Lagging Semis Since 2019

While portions of the software universe may face lasting business model impairment, we believe the recent indiscriminate selling across software will also create attractive opportunities for long-term investors. We recently initiated a position in Synopsys (SNPS), one of the world’s leading EDA (electronic design automation) software providers. In our view, the company remains well positioned to benefit from healthy semiconductor design activity, while its software offering faces a limited risk of near-term AI disruption. LCG also has a large position in Microsoft (MSFT), which we believe will emerge as a long-term AI winner despite recent underperformance. While JAG’s process is not designed to time bottoms, we continue to closely monitor the space and will not hesitate to opportunistically increase exposure in the event business prospects and investor sentiment show meaningful improvement. Based upon our experience, this is likely to take several quarters to play out.

Thank you for your interest in JAG Capital Management. We look forward to the opportunity to engage further.

– JAG’s Growth Equity Research Team