A thoughtful 401(k) plan audit is no longer just a compliance exercise, it’s a critical responsibility for today’s business leaders. Strong governance extends far beyond financial reporting and executive oversight. One of the most impactful, and often overlooked, duties leaders carry is ensuring their retirement plan is regularly reviewed and aligned with employees’ best interests.

For many employees, their 401(k) represents the cornerstone of their long-term financial future. For employers, it is both a meaningful benefit and a fiduciary obligation. When properly managed, a 401(k) plan can do more than meet regulatory requirements, it can strengthen culture, reduce risk, and play a key role in attracting and retaining top talent.

Understanding Fiduciary Responsibility Under ERISA

Under ERISA (the Employee Retirement Income Security Act), employers that sponsor a retirement plan act as fiduciaries. This means leaders are expected to act prudently, monitor the plan consistently, and make decisions solely in the best interest of participants.

Regular plan reviews—and when appropriate, a formal 410 (k) plan audit—help ensure these responsibilities are met.

Good governance is not about perfection—it’s about process. Leaders should be able to clearly articulate:

- How plan fees are monitored and benchmarked

- How investment options are selected and reviewed

- How decisions are documented and revisited over time

Without a structured process, even well-meaning organizations can expose themselves to unnecessary risk.

How a 401(k) Plan Audit Supports Attraction and Retention

Today’s workforce is paying closer attention to benefits, especially retirement plans. A competitive, well-managed 401(k) can be a meaningful differentiator when candidates evaluate job offers. This starts with a 401 (k) plan audit.

Prospective employees often compare:

- Employer matching contributions

- Investment quality and diversification

- Simplicity and accessibility of the plan

- Confidence that leadership is actively overseeing the program

A strong retirement plan sends a clear message: leadership is invested in employees beyond their immediate role.

For current employees, consistent oversight can reduce financial stress and reinforce long-term loyalty. Employees who trust their employer to safeguard their future are more likely to stay engaged and committed over time.

Key Areas Leaders Should Review In Their 401(k) Plan Audit

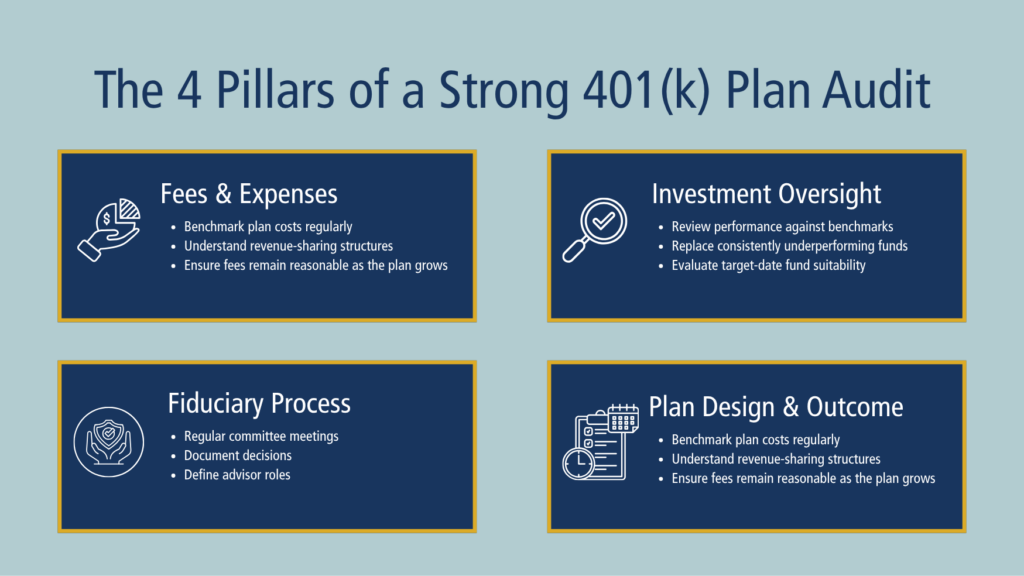

Plan Fees and Expenses

Fees matter—and are often more than employees realize. Leaders should periodically:

- Benchmark recordkeeping and investment fees

- Understand revenue-sharing arrangements

- Confirm costs remain reasonable as the plan grows

Even modest fee reductions can significantly improve long-term retirement outcomes.

Investment Oversight

A strong plan includes a diversified, well-monitored investment lineup. Best practices include:

- Reviewing performance against benchmarks

- Addressing underperforming funds

- Monitoring target-date fund suitability

Consistent oversight supports both fiduciary responsibility and participant confidence.

Fiduciary Process and Documentation

Regulators focus heavily on process. Leaders should ensure:

- Regular fiduciary or committee meetings

- Clear documentation of decisions and rationale

- Defined roles for advisors and service providers

Strong documentation protects both the organization and its leadership.

Plan Design and Employee Outcomes

Beyond compliance, leaders should evaluate whether the plan is truly helping employees succeed by reviewing:

- Participation and deferral rates

- Effectiveness of employer match structures

- Use of features like auto-enrollment and auto-escalation

Plans designed with employee behavior in mind often lead to stronger outcomes and higher engagement.

Turning Oversight Into Opportunity

According to the IRS 401(k) Resource Guide, regular plan reviews are no longer just a regulatory necessity—they’re an opportunity to strengthen governance, improve employee outcomes, and support long-term business success.

For leaders who want to ensure their retirement plan aligns with their values, workforce goals, and fiduciary responsibilities, establishing a consistent review process is an important first step.

With the right guidance and perspective, what begins as a requirement can become a strategic advantage—for both the organization and its employees.