March 2026

Investing in Transformation That Matters

Why Your Mortgage Rate Isn’t Just About the Fed

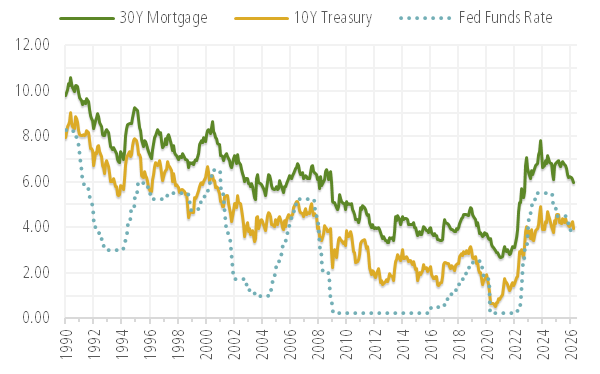

The 10-Year, Not the Fed Funds Rate

The Federal Reserve controls the overnight lending rate. That rate anchors the front end of the yield curve and cascades to savings accounts, money market funds, and short-term CDs.

A 30-year mortgage is an entirely different animal. The investors who ultimately fund these loans, primarily via mortgage-backed securities (MBS), are committing capital for decades, not days. Their reference point is the 10-year US Treasury yield, which has long served as the de facto benchmark for 30-year mortgage pricing. The 30-year Treasury bond might seem like a more intuitive match, but because mortgages amortize and borrowers prepay, the effective duration of a mortgage portfolio sits closer to the 10-year.

Exhibit 1: 30-Year Fixed Mortgage Rate vs. 10-Year Treasury Yield vs. Fed Funds Rate

The Spread on Top

Even the 10-year Treasury does not tell the whole story. Mortgage rates carry an additional spread above that benchmark, compensation to lenders and investors for risks unique to the mortgage market. Those risks include the possibility that homeowners refinance when rates fall (prepayment risk), general credit considerations, and the liquidity characteristics of mortgage-backed securities. The components differ from those we analyze as corporate bond investors, but the framework is consistent: higher risk demands higher spread, and risk appetite is fluid.

At times, both spreads move together, as periods of broad market stress tend to widen risk premiums across asset classes simultaneously. But Exhibit 2 reveals that a gap emerged in 2022 and has persisted. Mortgage rates were pushed higher during this period by both a rising 10-year yield and an unusually wide spread. The Federal Reserve, through quantitative easing, had been a significant buyer of mortgage backed securities for much of the prior decade — a tailwind for mortgage spreads that reversed when the Fed began shrinking its balance sheet in 2022. Some normalization in mortgage spreads, if and when it occurs, could provide modest relief on mortgage rates.

Exhibit 2: Mortgage Spread vs. Corporate Bonds and Fed MBS Holdings

What Moves the 10-Year?

If the 10-year is the anchor, what moves the anchor? Primarily inflation expectations. When the market believes inflation will persist, long-term yields rise. When it expects inflation to moderate durably, yields can fall, sometimes before the actual data confirms it.

Exhibit 3: Inflation Expectations and Mortgage Rates

Source: Bloomberg Finance LP, JAG Capital Management

Elevated inflation uncertainty feeds directly into rate volatility, and rate volatility makes prepayment behavior significantly harder to model. Mortgage investors demand additional spread compensation as a result. The relative calm in rates of late, if sustained, removes at least one of the factors that has kept mortgage spreads stubbornly elevated since 2022.

What Would It Take?

Mortgage rates breaking durably below 6% would likely require some combination of a sustained decline in inflation expectations, a meaningful compression of the mortgage spread back toward historical norms, or an economic slowdown significant enough to drive a genuine flight to Treasuries.

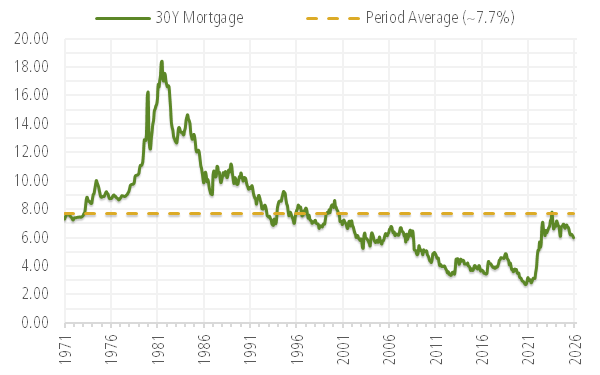

Exhibit 4: 30-Year Fixed Mortgage Rate — 1971 to present

None of this makes the current rate environment comfortable for prospective homebuyers. But understanding the mechanics — Treasury yields, inflation expectations, and the spread layered on top — reframes the question from “why hasn’t the Fed fixed this?” to a more precise and answerable one: what would need to change in each of those components?

As bond investors, we ask a version of that question every day. The instruments are different; the framework is the same.

– JAG’s Fixed Income Research Team