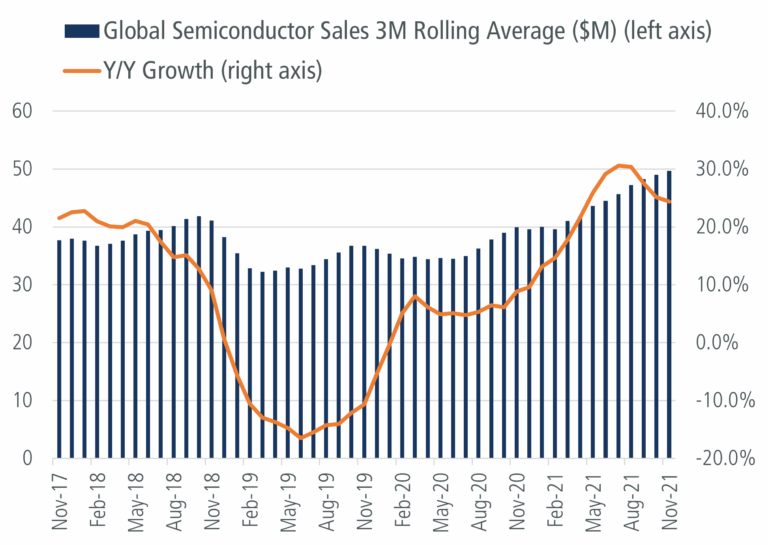

January 6, 2022 — Global semiconductor sales continue to trend upward, growing close to +24% year over year in November 2021 (Figure 1). The strong demand environment is a byproduct of several factors, including robust personal computer (PC) sales due to work-from-home initiatives, rising demand from applications such as data center and high-performance computing (HPC), and ongoing 5G deployment globally. Meanwhile, well-documented supply shortages continue to drive favorable pricing for semiconductor makers. While supply conditions are improving, demand continues to outstrip supply and most semiconductor companies expect shortages to last well into 2022 (and possibly 2023).

While the semiconductor industry remains cyclical and is subject to short-term demand volatility as well as regulatory risks, we see the industry well positioned moving forward due to several factors:

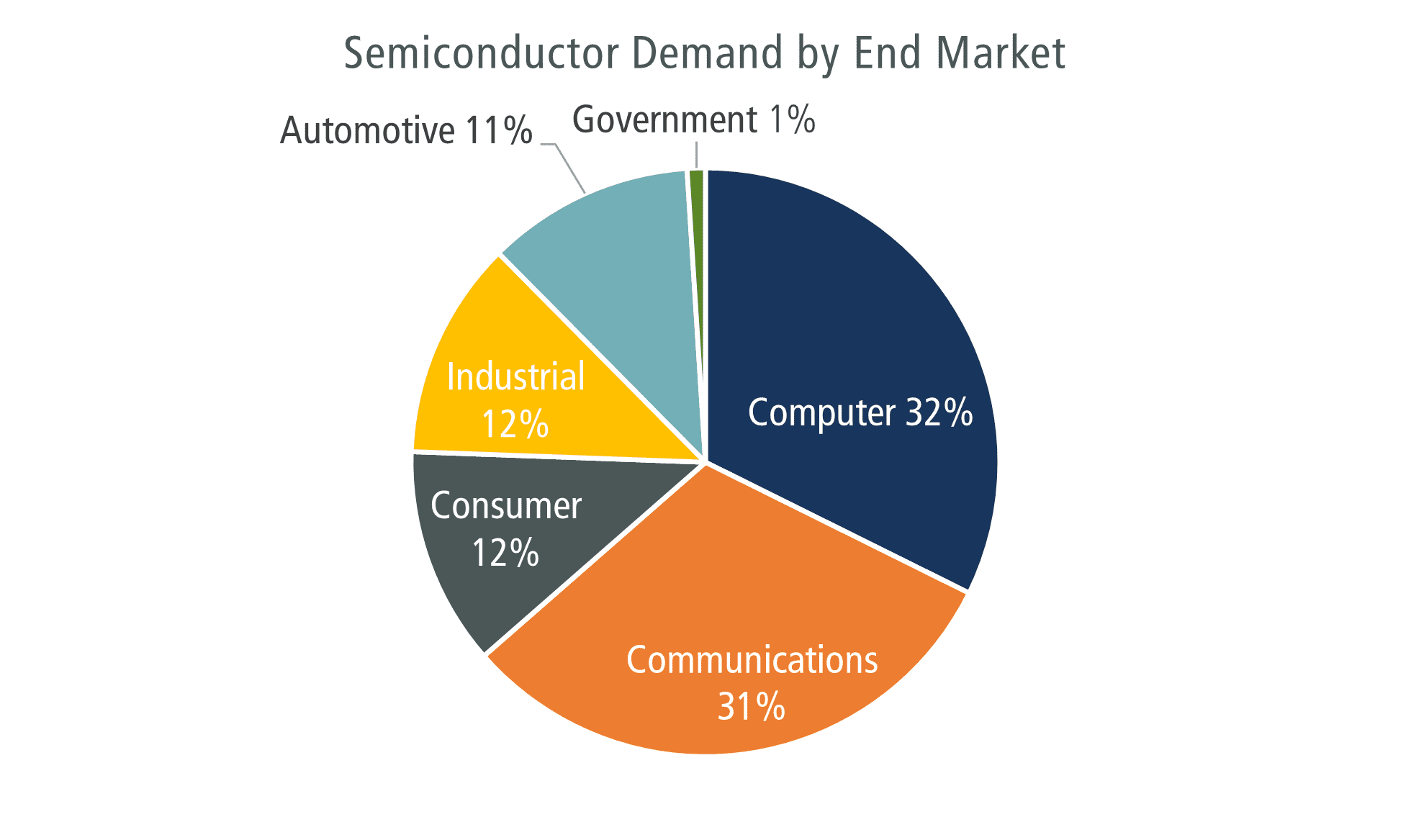

- More Growth Levers: Historically, the PC segment accounted for a lion’s share of semiconductor end use and semiconductor sales tended to exhibit high cyclicality depending on the PC demand environment. However, with the emergence of new, rapidly growing technologies such as HPC, autonomous driving and Internet of Things (IoT), cyclicality has decreased as semiconductor sales are not overly reliant on any single end market (Figure 2).

- Better Visibility: While the current supply shortage is limiting semiconductor makers’ revenue upside, many customers are signing long-term contracts to avoid future supply-related disruptions. Increased demand visibility should allow for more predictable revenue streams and better capital allocation decisions.

- Industry Consolidation: The semiconductor industry has seen increased consolidation as manufacturing complexity and costs continue to rise. For example, currently there are only a few leading-edge chip makers (Taiwan Semiconductor Manufacturing, Intel, Samsung) as other foundries left the race due to high costs and technological complexity. The memory chip market has also become more concentrated, with Samsung, SK Hynix, and Micron Technology accounting for roughly 95% of global market share according to Statista. Higher concentration should lead to a better pricing environment as chip makers are more disciplined in adding supply.

Rapidly growing semiconductor demand and the current shortage has also incentivized higher capital investments into capacity expansions. For example, Taiwan Semiconductor Manufacturing (TSMC) announced it will spend $100B over the next three years, Intel is investing $20B in two chip plants, and Samsung announced it will spend $17B to build a factory in Texas. Coupled with higher capital intensity as we transition towards even smaller chips (TSMC expects to start volume production of its 3nm technology in 2022), these trends should also broadly benefit semiconductor equipment companies as their tools are vital in the chip manufacturing process.

JAG’s investment approach helps us identify great companies that can capitalize on durable sector and industry-specific trends and opportunities. We welcome your comments and questions any time!

– George Margvelashvili, CFA®, JAG Investment Team